Latest Update: The PM Vidyalaxmi portal has already sanctioned over 60,600 loans worth approximately Rs 7,755 crore as of February 24, 2026. Applications are open right now at pmvidyalaxmi.co.in.

Collateral. Guarantors. These two words have killed the higher education dreams of more Indian students than we’d like to admit. You get into a good college, you’ve worked hard for it, and then the bank asks your family to mortgage the house. For what? To prove you’re serious about studying?

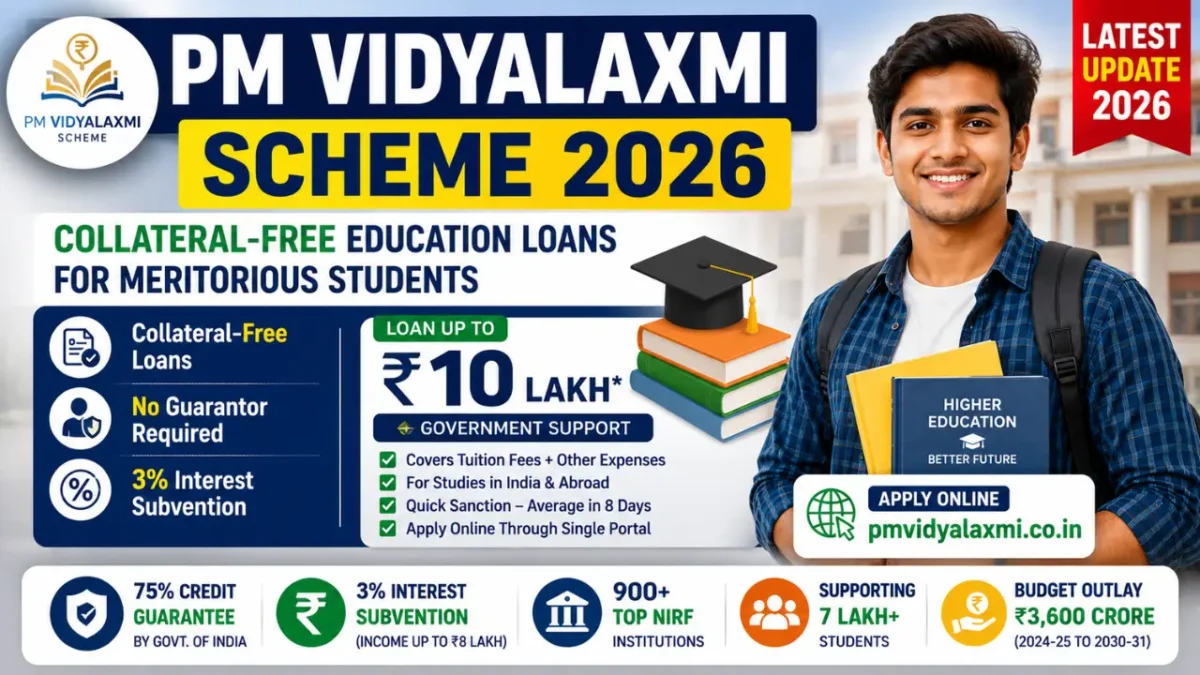

The PM Vidyalaxmi Scheme was built to fix exactly that. Approved by the Union Cabinet on 6 November 2024, it offers collateral-free, guarantor-free education loans to students who earn merit-based admission into top-ranked institutions in India. No property pledging. No FD as security. Just your admission letter and a digital application.

What Is the PM Vidyalaxmi Scheme, Exactly?

It’s a Central Sector scheme that runs through a single digital portal: pmvidyalaxmi.co.in. Students apply there, choose their bank, upload documents, and track the whole process online. Banks are more willing to sanction these loans because the government provides a 75% credit guarantee on loans up to Rs 7.5 lakh. That’s the key mechanism here. The risk shifts away from the family.

On top of that, students from families earning up to Rs 8 lakh per year get a 3% interest subvention during the moratorium period on loans up to Rs 10 lakh. So you’re not just getting a loan, you’re getting a cheaper loan, with the government absorbing part of the interest while you’re still studying.

The government has set aside Rs 3,600 crore for this scheme between 2024-25 and 2030-31. It’s built to support around 7 lakh fresh students over that period.

Key Highlights at a Glance

| Feature | Details |

|---|---|

| Scheme Type | Central Sector Scheme |

| Cabinet Approval | 6 November 2024 |

| Loan Nature | Collateral-free, Guarantor-free |

| Credit Guarantee | 75% by Govt. of India (up to Rs 7.5 lakh) |

| Interest Subvention | 3% on loans up to Rs 10 lakh (income up to Rs 8 lakh) |

| Expenses Covered | Tuition fees + course-related expenses |

| Study Location | India and Abroad |

| Official Portal | pmvidyalaxmi.co.in |

| Total Budget | Rs 3,600 crore (2024-25 to 2030-31) |

| Institutions Covered | 900+ QHEIs and expanding |

Who Can Actually Apply?

Let’s break this into two parts: who the student needs to be, and which colleges are covered.

For the student:

- Indian citizen

- Admission through merit or a recognised entrance exam

- Pursuing UG, PG, diploma, or integrated courses

- Any income group can apply for the loan itself

- For the 3% interest subvention, family income should be up to Rs 8 lakh per year

For the institution (called QHEIs):

| Institution Type | Condition |

|---|---|

| Govt. and Private HEIs | Top 100 in NIRF (overall or category-specific) |

| State Govt. HEIs | Ranked 101-200 in NIRF |

| Central Govt. Institutions | All institutions covered |

The QHEI list started at 860 institutions when the scheme launched and has since crossed 900 with additions of constituent colleges. It’s updated every year based on fresh NIRF rankings, so don’t just go by what you read somewhere six months ago. Check the official portal for the current list before applying.

Also Check: Latest Bihar Board 12th Compartmental Result 2026 Declared – Check Your BSEB Inter Score Right Now

The Benefits, In Plain Terms

- No collateral needed for loans up to Rs 7.5 lakh. The government backs it.

- 3% interest subvention during moratorium for income up to Rs 8 lakh (on top of existing CSIS benefits for those under Rs 4.5 lakh)

- Full tuition fees covered, plus other course-related expenses

- Works for studies in India and abroad

- Average loan sanction time has come down to under 8 days in recent data

- You can apply to multiple banks through the same portal and compare

That last point matters more than people realise. In a normal bank visit, you don’t really get to compare offers easily. Here, the platform lets you see options and choose.

Documents You’ll Need

Keep these ready before you start the application. It saves a lot of back-and-forth later.

- Class 10 marksheet

- Class 12 or last qualifying exam marksheet

- Admission or offer letter from your college

- Fee structure or expense schedule from the institution

- Family income proof from a public authority

- Applicant and parent photographs

- Aadhaar, PAN, and address proof

Some documents already submitted to the college can be accepted with a certificate from the institution. But this varies by bank, so confirm before assuming.

How to Apply: Step by Step

- Go to pmvidyalaxmi.co.in

- Register with your mobile number and email

- Log in and fill the Common Education Loan Application Form (it’s a two-page form, not complicated)

- Upload the required documents

- Select one or more banks

- Submit and track your application

- Once sanctioned, visit the bank branch for final formalities

The whole thing is online up to the last step. Most students who keep their documents ready report a smooth experience.

How Is the Scheme Performing So Far?

As per data released in March 2026, covering activity up to 24 February 2026:

| Metric | Figure |

|---|---|

| Applications under PM-Vidyalaxmi | Over 1 lakh |

| Loans Sanctioned | Around 60,600 (approx. 60%) |

| Amount Sanctioned (scheme) | Around Rs 7,755 crore |

| Total Portal Applications (all schemes) | Nearly 6.5 lakh |

| Total Loans Sanctioned (all schemes) | Over 3.3 lakh |

| Total Amount Sanctioned (all schemes) | Approx. Rs 36,000 crore |

A 60% sanction rate in year one is a solid start. It’s not perfect, but it shows the system is working and improving. The average processing time coming down is especially important for students who need confirmation before semester deadlines.

Why This Actually Matters for Students and Families

Here’s the real-world picture. A student from a middle-class family in, say, a Tier 2 city cracks JEE or NEET, gets into a reputed private college, and then the loan conversation starts. The bank asks for property papers. The parents don’t have anything substantial to offer. The student either drops the seat or takes a high-interest personal loan from somewhere informal.

That situation is what this scheme is trying to end. And it’s not just about accessing money. Studying at a top NIRF-ranked college genuinely changes career outcomes. Better placements, stronger networks, higher starting packages. The education investment makes more sense when you can actually access the institution.

So yes, the long-term return on this scheme, for eligible students who use it well, is significant.

Important Links

| Resource | Link |

|---|---|

| Apply Online | pmvidyalaxmi.co.in |

| MyScheme Page | myscheme.gov.in/schemes/pmvs |

| Education Ministry | education.gov.in |

Final Thoughts

The PM Vidyalaxmi Scheme won’t solve every problem in Indian higher education financing. It doesn’t cover every college, and it won’t help students in institutions outside the NIRF list. But for those who do qualify, it’s genuinely one of the better-designed schemes in recent years. Simple process, digital-first, with a real financial safety net built in.

If you or your child has a seat in a QHEI, don’t wait. Visit the portal, check the current institution list, and start the application. Keep the admission letter and fee structure ready from day one.

And if you’ve already been through this process, or you’re about to apply this academic year, share your experience below. What was the bank processing like? Did you face any delays? Practical inputs from real applicants help others more than any official guide can.

FAQs

Who is eligible for the PM Vidyalaxmi Scheme?

Simply put, if you’ve got a merit-based seat in a NIRF-ranked college, you can apply. Income doesn’t matter for the loan itself. But if you want the 3% interest subvention, your family income needs to be under Rs 8 lakh per year. Check the QHEI list on the portal first because not every college qualifies.

How much interest on a 20 lakh education loan?

The subvention benefit only applies up to Rs 10 lakh, so a Rs 20 lakh loan won’t get full coverage. The actual rate depends on whichever bank you pick through the portal. Compare a few options before deciding, because rates do vary.

When did the PM Vidyalaxmi Scheme start?

The Cabinet approved it on 6 November 2024 and the portal went live soon after. By early 2026, it had already crossed 1 lakh applications. So it’s not new anymore, it’s running and sanctioning loans actively.

Is the Vidyalaxmi loan interest free?

Not entirely, but close for many families. If your income is under Rs 8 lakh, you get a 3% subvention during the moratorium period. Under Rs 4.5 lakh? The existing CSIS scheme covers the full interest. So depending on where your family falls, the actual out-of-pocket interest cost can be quite low.